This article will help you to understand the basics of limited companies and take you through each step you need to complete in order to set up your very own limited company.

What is a limited company?

First things first, it is important to understand exactly what a limited company is. There are two types of limited companies.

Limited by shares – businesses that make a profit, meaning:

- They are legally detached from the people who run it

- Their finances are separate from personal

- There will be shares and shareholders

- The profits can be kept after paying tax

Limited by guarantee – known as ‘not for profit’, meaning:

- They are legally detached from the people who run it

- Their finances are separate from personal

- There will be guarantors and a ‘guaranteed amount’

- The profits made will be invested back into the company

- Check if setting up a limited company is the best thing for you

The way you set up your business depends on the work you do, it also has an effect on the way you pay taxes and receive funding.

The fundamental reasons for choosing to trade as a limited company are limited liability, tax efficiency, and professional status. However, there are several other advantages and disadvantages:

Advantages of setting up a limited company

- Your personal assets will be secure – Limited companies have limited liability protection meaning that if your company gets into trouble, your personal assets will remain secure, as you will be treated as a separate legal entity.

- Professional status – Limited companies are held in much higher regard and create a better impression.

- Tax efficiency and planning – If you trade as a limited company in the UK, you have to pay 19% Corporation Tax on profits. If you trade as a sole trader, you are required to pay 20-45% Income Tax on your profits.

Disadvantages of setting up a limited company

- Fees – You will need to pay an incorporation fee to Companies House

- Visibility – Personal and corporate information will be disclosed on public record

- Time & Stress – Accounting requirements are more complicated and time-consuming – learn more about how Wise helps you to save time and money. [link to save time and money blog]

- Find a name

Choosing a name for your business is not as easy as you may initially think, you need to make sure you check the rules for company names, check if the name you want is available and also check if existing trademarks exist. You may also want to check on domain name service providers (such as GoDaddy) and other social platforms to see if your name is available.

- Appoint directors and a company secretary

You must ensure that you appoint a director, but it is not necessary that you appoint a company secretary.

- Agree on who the shareholders or guarantors will be

You will need to find at least one shareholder or guarantor, who will also be a director.

- Establish people who have significant control (PSC) over your company

A person with significant control (PSC) is a person who owns or manages your company, sometimes known as ‘beneficial owners’. It is important to tell Companies House who your PSC’s are.

- Create documents agreeing on how to run your company

It is essential you register a ‘memorandum of association’ (a legal document signed by all initial shareholders or guarantors agreeing to start the company) and an ‘articles of association’ (written rules about managing the business agreed by shareholders or guarantors, directors and the business’ secretary).

- Find out what records you’ll need to keep safe

You must keep records about the company itself and financial and accounting records.

Company records include:

- Directors, shareholders and company secretaries

- The results of shareholder votes and resolutions

- Promises for the company to repay loans and who they must be paid to

- Promises the company makes for payments if something goes wrong and it’s the companies fault

- Transactions – relating to if anyone purchases shares in the company

- Loans or mortgages against the company’s assets

Accounting records include:

- Money spent by the company e.g. receipts, orders, delivery notes etc

- All money received by the company e.g. contracts, sales books, till rolls etc

- Any other relevant documents e.g. bank statements and correspondence

- Register your company

You will need to register an address and choose a SIC code (this identifies what your company does).

The majority of people will register for Corporation Tax at the same time as registering with Companies House. If you can’t, you will need to register separately with HMRC after you have registered with Companies House.

As a driver with Wise, you will receive the following benefits:

- A quick, smooth onboarding process

- Better communication

- Education and protection around employment status

- Compliance reassurance

- Access to discounted invoicing & accountancy services

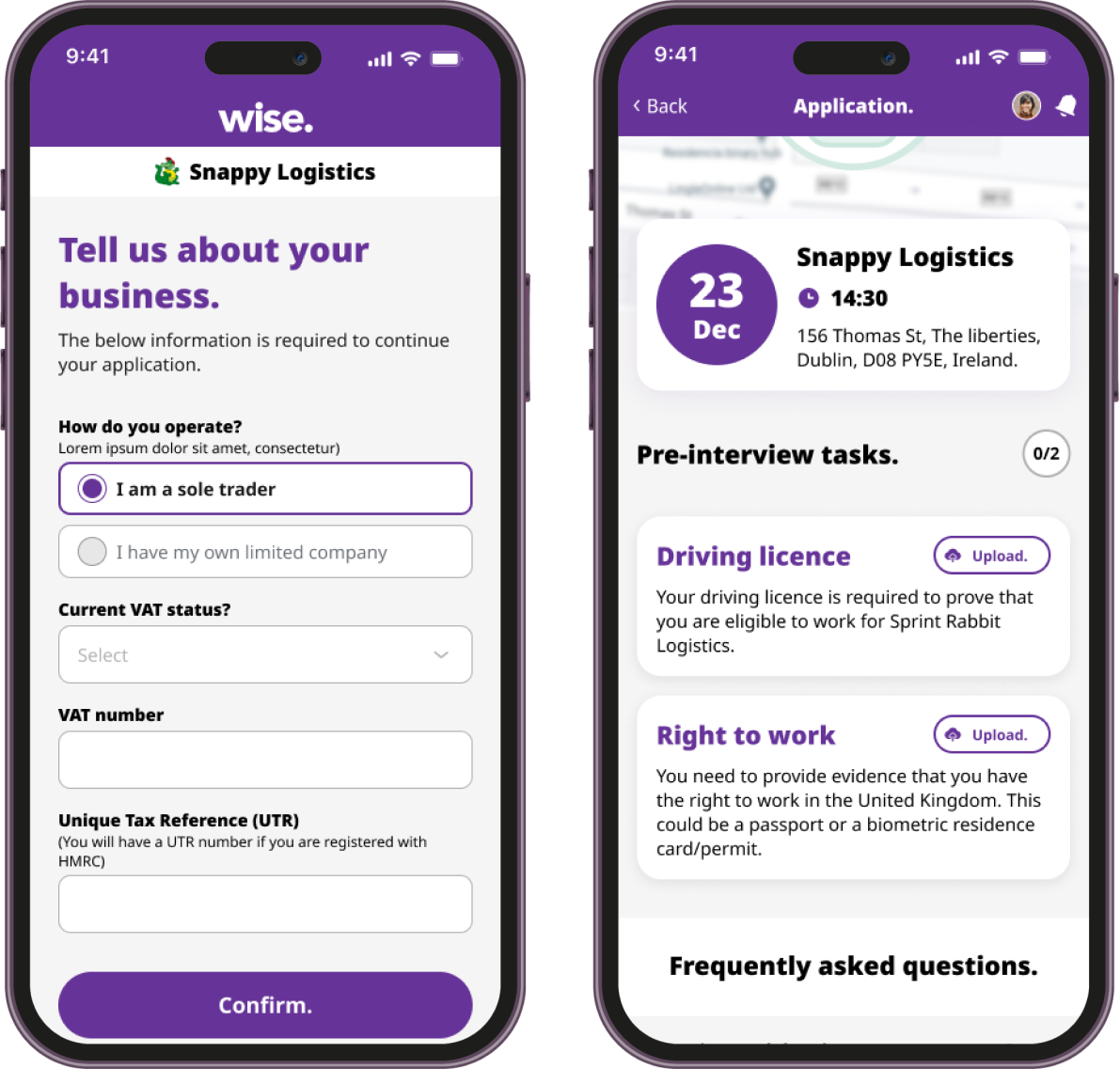

As a business owner with Wise – Our software and services, help you with:

- Compliance: Protection from the HMRC gives you peace of mind and reduces stress

- Onboarding: Faster and streamlined onboarding thanks to our app saves you time and allows your drivers to get on the road ASAP.

- Payments technology: Easy setup and scheduling of payments, powered by Modulr, allowing you more time to focus on the growth of your business

To find out more about what Wise offers contact us or book a demo.